Blog

What is Disability & Long-Term Care Insurance? Coverage Options in BD

Life has a way of shifting gears when you least expect it. While many professionals and business owners carefully secure their tangible assets, they often overlook their most valuable asset: their personal ability to earn an income.

If a serious illness or severe accident suddenly takes away your physical or mental capacity to work, the financial fallout can be immediate. In the local market, safeguarding against these specific health crises falls under two distinct categories: Disability Insurance and Long-Term Care (LTC) Insurance.

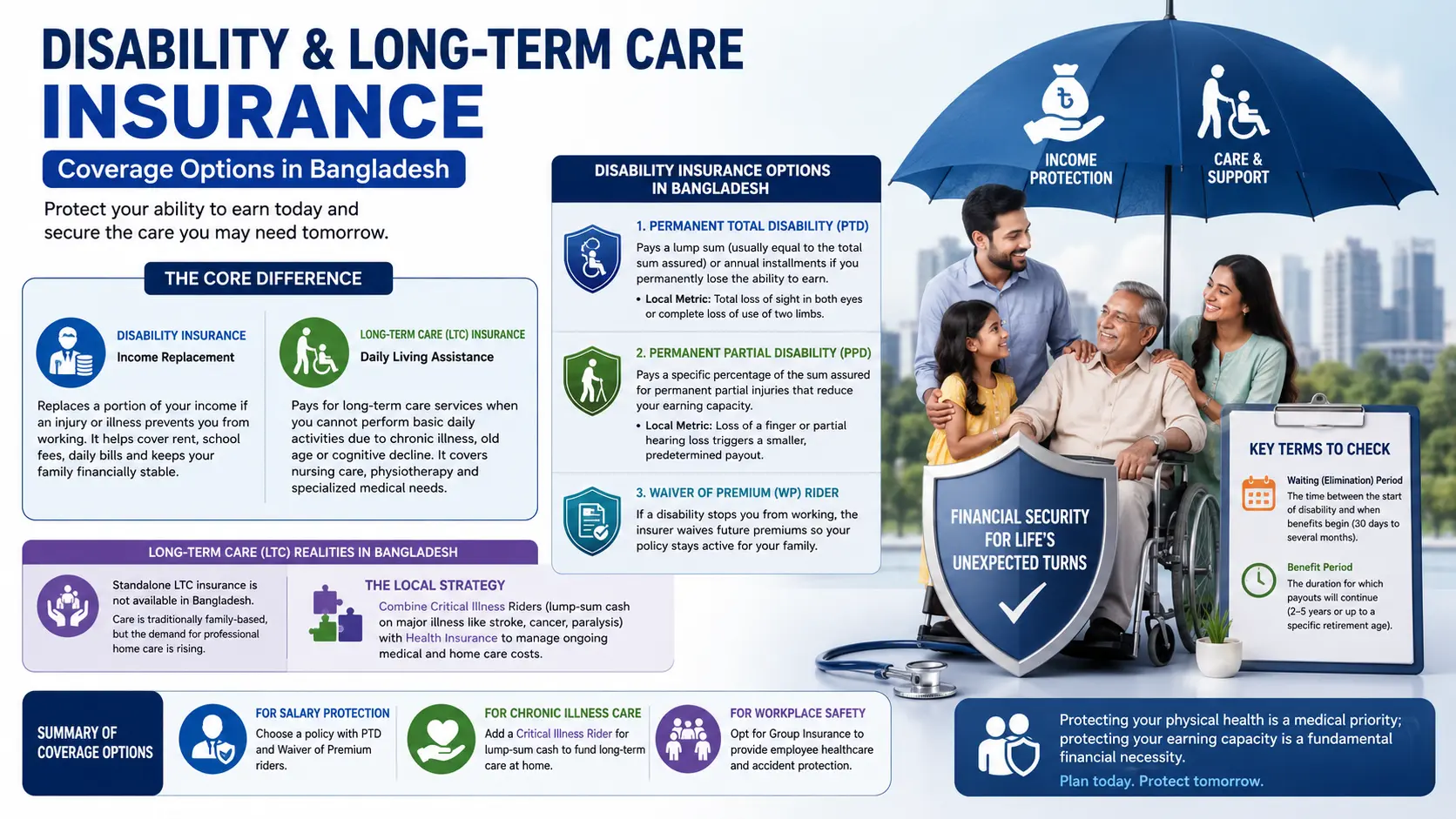

The Core Difference: Income Replacement vs. Daily Living Assistance

While both policies step in during a severe medical crisis, they serve entirely different financial functions.

- Disability Insurance acts as an income substitute. It replaces a portion of your monthly salary or business revenue if an injury or medical condition prevents you from performing your regular professional duties. It keeps your family afloat by covering rent, school fees, and daily bills.

- Long-Term Care (LTC) Insurance acts as a care funding mechanism. It pays for the physical assistance required when a chronic medical condition, cognitive decline, or old age renders you unable to perform basic daily routines. It covers the costs of private home nurses, physiotherapy, or specialized medical equipment.

Disability Insurance Options in Bangladesh

In the Bangladeshi insurance sector—regulated by the Insurance Development and Regulatory Authority (IDRA)—standalone, long-term disability policies are rare. Instead, disability protection is primarily structured as a Rider (an optional, paid add-on) attached to a comprehensive individual policy or a corporate workplace policy.

1. Permanent Total Disability (PTD)

This coverage triggers if an illness or accident results in a permanent condition that completely ends your ability to earn a living ever again.

- Typical Payout Structure: Usually distributed as a tax-free, single lump-sum payment (often matching the total sum assured of the main life insurance in Bangladesh), or broken down into guaranteed annual installments over a fixed period.

- Local Metric: Insurers look for irreversible conditions, such as the total loss of sight in both eyes, or the complete loss of use of two limbs.

2. Permanent Partial Disability (PPD)

This applies when an accident causes a permanent injury, but you are still capable of performing certain types of light work or modified professional duties.

- Typical Payout Structure: The insurer pays out a specific percentage of the total sum assured based on a scale of injury severity.

- Local Metric: For instance, losing a single finger or sustaining partial hearing loss will trigger a smaller, predetermined percentage payout to help offset your reduced future earning potential.

3. Waiver of Premium (WP) Rider

This is a highly recommended safety net for long-term policyholders. If you suffer a validated disability that stops you from working, this clause steps in to ensure your core financial plan does not lapse. The insurance company waives all future premium payments, keeping the policy fully active for your family.

Long-Term Care (LTC) Realities in the Local Market

Traditional, standalone long-term care insurance—common in Western markets to cover nursing homes—does not exist in a structured form within Bangladesh. Culturally, care for the elderly or chronically ill has deeply relied on the family network.

However, as urban corporate lifestyles rise and nuclear families become more common in major cities, the financial demand for professional healthcare at home has surged. Locally, managing these costs relies on alternative insurance structures:

- The Local Strategy: To manage long-term medical care costs in Bangladesh, individuals combine Critical Illness Riders (which provide a lump-sum cash payout upon diagnosis of strokes or paralysis) with foundational health insurance in Bangladesh packages that handle ongoing hospitalization and diagnostic test bills.

Critical Illness Riders as an LTC Alternative

When you add a Critical Illness Rider to your policy, it covers a specified list of major medical conditions (such as advanced cancer, major strokes, kidney failure, or paralysis).

Upon a confirmed clinical diagnosis, the company gives you a direct cash payout. You are completely free to use this money to hire private home care nurses, purchase specialized medical equipment, or fund long-term physical therapy sessions.

Key Terms to Check Before Signing

Before choosing an option, look closely at these two hidden operational timelines in the policy document:

- The Waiting (or Elimination) Period: This is the pocket of time between the initial day your disability starts and the actual day the insurance provider begins paying out benefits. This can range from 30 days to several months. You will need enough personal emergency savings to cover your expenses during this gap.

- The Benefit Period: This defines how long the insurance payouts will keep coming. Some policies only cover a short block of time (like two to five years), while others extend payouts until you reach a specific retirement age.

Summary of Coverage Options

- For Salary Protection: Secure a personal baseline policy optimized with both Permanent Total Disability (PTD) and Waiver of Premium riders.

- For Chronic Illness Care: Attach a comprehensive Critical Illness Rider to access a lump-sum cash fund if you ever need to set up intensive medical care at home.

- For Workplace Safety: If you are managing an enterprise, looking into structured corporate solutions that bundle employee healthcare with accident protection through group insurance in Bangladesh is the most efficient way to safeguard your team.

Protecting your physical health is a medical priority; protecting your earning capacity is a fundamental financial necessity. Taking time to review your policy options ensures that a sudden medical crisis won't derail your family's financial stability.